No Valuation Bridging Loans

Fast short-term property finance across England, Wales and Scotland without a full inspection valuation. From 0.55% per month, up to 75% LTV.

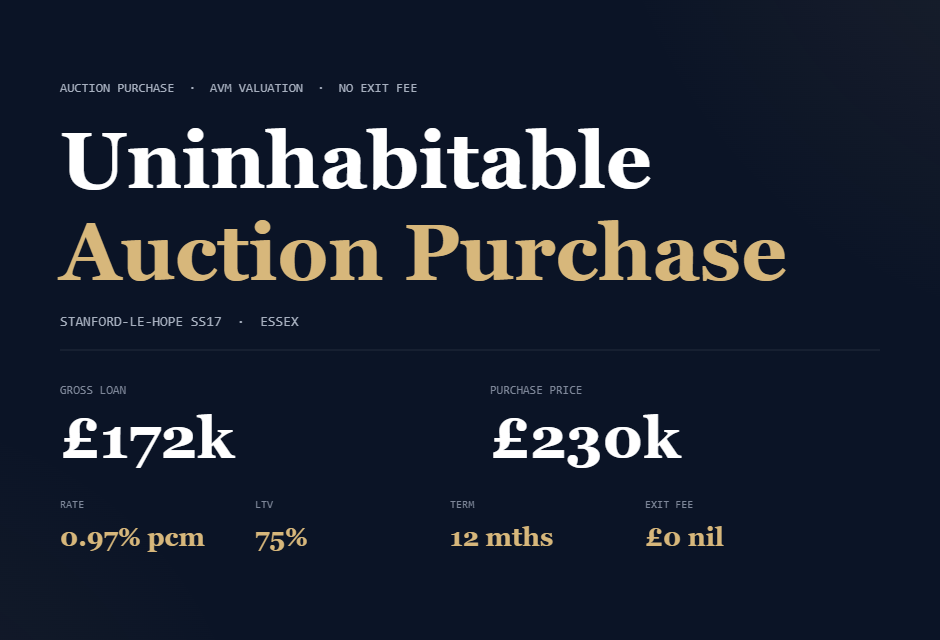

Common use cases: auction purchases, refinance, chain breaks, standard residential assets and time-sensitive acquisitions.

No valuation bridging loans are short-term property loans where the lender does not rely on a full internal inspection valuation, instead using AVM, desktop or internal valuation methods to assess the property and move faster.

They are designed for speed and flexibility where a traditional full valuation would slow the deal down - particularly on standard properties, low-to-mid LTV cases and time-sensitive purchases or refinances.

- Rates: from 0.55% per month

- Maximum LTV: up to 75% (case dependent)

- Loan terms: typically 3-24 months

- Borrowers: individuals, limited companies and SPVs

- Use cases: purchases, auctions, refinance, chain breaks and selected refurbishment-backed exits

Related products: AVM bridging loans, desktop valuation bridging loans, auction finance, light refurbishment bridging loans, refurbishment bridging loans, bridging loans for bad credit.

What is a no valuation bridging loan?

A no valuation bridging loan is short-term property finance where the lender does not require a full physical inspection valuation before offering funds. Instead, the lender usually relies on quicker alternatives such as AVM bridging loans, desktop valuation bridging loans or an internal assessment using comparable evidence and its own underwriting.

Borrowers commonly use no valuation bridging finance when speed matters, the property is straightforward, and there is a clear exit such as sale or refinance. It is often relevant for auction finance, investment purchases, urgent refinancing and lower-risk cases where a full valuation adds time without materially improving lender comfort.

Can I qualify?

Most no valuation bridging cases are assessed on property type, leverage, borrower profile and exit strength. This section makes the main eligibility questions easier to scan.

No valuation does not mean no underwriting. Lenders still need to be comfortable with the security, the evidence supporting value, and the planned exit. Straightforward residential properties tend to fit best, while more specialist assets may need a different route such as commercial no valuation bridging, commercial bridging loans or a full valuation-backed structure.

Usually considered

Standard houses and flats, limited companies and SPVs, auction purchases, lower to mid-LTV refinances, simple titles and many adverse credit scenarios.

Usually more lender-specific

Heavy refurbishment, highly unusual assets, complex titles, specialist commercial property, second charge cases and weaker or unproven exits.

| Question | Typical answer | What helps |

|---|---|---|

| Ltd Co / SPV? | Yes | Company docs and directors ready |

| Bad credit? | Often yes | Lower LTV and stronger exit |

| Auction purchase? | Yes | Legal pack and deposit ready |

| Standard residential asset? | Often yes | Good comparable evidence |

| Commercial property? | Sometimes | May suit commercial no valuation bridging |

| Heavy refurbishment? | Case dependent | May need a specialist works-based structure |

What will it cost?

Rates are monthly. Total cost depends on LTV, borrower profile, property simplicity, valuation route and exit strength.

Pricing can vary depending on whether the lender is comfortable with an AVM bridging loan, a desktop valuation, or an internal assessment. More complex assets may be better suited to no valuation heavy refurbishment bridging, refurbishment bridging loans or a more bespoke commercial bridging loan structure where the asset profile requires it.

Low LTV, clean credit, straightforward residential asset and strong refinance or sale exit. Indicative range: 0.55% to 0.69% pm.

Standard purchases, refinances and auction cases using AVM, desktop or internal valuation routes. Indicative range: 0.69% to 0.95% pm.

Bad credit, specialist property, second charge or less straightforward exits. Indicative range: 0.95% to 1.20% pm+.

Arrangement fee typically 1.5% to 2%, plus legals and admin fees depending on lender and structure. Upfront valuation costs may be reduced versus a full inspection route.

| Term | Range | What it means |

|---|---|---|

| LTV | Up to 75% | Higher leverage usually means higher pricing and tighter exit scrutiny. |

| Loan size | £26,000 to £10m | Higher available in some cases. |

| Term | 3 to 24 months | Should match the refinance, sale or stabilisation timeline. |

| Interest type | Retained, rolled or serviced | Retained reduces day-one net advance. Serviced requires monthly payments. |

| Arrangement fee | 1.5% to 2% typical | Often added to the facility or deducted on completion. |

How fast?

Speed depends on the valuation route, solicitor responsiveness, document readiness and whether the deal is straightforward or specialist.

The biggest advantage of no valuation bridging is that removing a full inspection report can materially reduce delay. In the right case, this can sit alongside closed bridging loans, investment purchase bridging loans, second charge no valuation bridging loans or equitable charge bridging loans depending on the borrower’s structure and security position.

What’s required?

We have simplified the enquiry path so users can start with a quick qualification form first, then complete a fuller pack once the case is confirmed as viable.

Where the asset or scenario is more specialist, related products such as permitted development finance, land bridging loans, commercial no valuation bridging, high value residential bridging loans or regulated bridging loans may also be relevant depending on the security and borrower circumstances.

Name, phone, email, postcode, property value and loan purpose. Enough to confirm feasibility and likely lender route.

Loan amount, term, exit, company details, credit profile, property information and supporting documents.

Purchase price, deposit position, legal pack or sales memo and target completion date.

Existing debt position, property background, refinance plan and broker AIP where available.

No valuation bridging loan questions answered

What does no valuation bridging loan actually mean?

It means the lender is not relying on a full physical inspection valuation report. Instead, it may use AVM data, a desktop report or its own internal valuation process to move faster.

Can I apply through a limited company or SPV?

Yes. This is one of the most common borrower structures. Directors' personal guarantees are typically required.

Can bad credit still be considered?

Often yes. Bridging is usually more asset-led than income-led, but recent severe issues or insolvency events can narrow the market.

How quickly can it complete?

Fast cases can move very quickly, especially where the asset is straightforward and the documents and solicitors are ready. Removing a full valuation can materially reduce delay.

Our Case Studies

Discover how we’ve helped clients secure fast, flexible funding across acquisitions, refinances, and development deals.